The capital engine behind every platform.

The $10B opportunity hiding inside Canada's platforms

Our Mission

We fuel small business growth

The Problem

An Etsy seller wants to grow their shop.

Seller

Without capital, they can't stock up or run ads. The shop sells less. Etsy makes less.

Seller

If Etsy could offer capital, both grow.

Unique Insight

Canada's platforms are sitting on the richest SME data.

That data makes them the perfect new distribution channel for capital — trusted by sellers, more efficient than banks, and impossible for existing fintech lenders to replicate.

The Power of Credit

Credit supercharges the platform growth flywheel.

Every platform wants to offer credit, but alone, they crash on execution.

Growth

Sellers Grow Faster

More capital

Retention Skyrockets

Platforms Earn More

The DIY Nightmare

Want to build lending yourself? Here's your Roadmap

Every platform thinks they can do it. Every platform suffers the same fate. Even Shopify relies on 3rd party for lending.

Research & Planning

Team Building

Banking Partners

Tech Build

Compliance

Underwriting Models

Launch & Scale

2-3 MONTHS

Regulatory maze

Legal consultants

Market analysis

Board convincing

3-4 MONTHS

15+ new hires

$2M+ salaries

Risk officers

Underwriters needed

4-5 MONTHS

20+ rejections

Debt facility

Due diligence

Terms negotiation

4-6 MONTHS

Decision engine

API integrations

Loan management system

Payment processing

3-4 MONTHS

KYC/AML systems

Provincial licenses

FINTRAC setup

Integration chaos

3-4 MONTHS

Model tuning

Default management

Collections setup

Never-ending costs

ONGOING

Constant iterations

Collections setup

Default management

Never-ending costs

Solution

Slate unlocks embedded lending in Canada

Platforms spend 6+ months and $500K+ to launch lending. Slate helps a platform launch in 24 hours.

Slate has 3 core products

We handle: Bank partner, Underwriting,

Servicing, Compliance & Risk Management.

Platforms

The Platform handles: Distribution, Customer Experience & Core Product.

Widgets

APIs

Ready to Launch

How It Works

Launch 'Shopify Capital' tomorrow, not next year.

Platforms no longer need bank partnerships, compliance teams & underwriting models - just plug us in and start fueling your customers growth with capital in days. Slate leverages our partners debt facility to extend capital.

Borrowers

Platform customers like

- Gig workers

- Online Shop owners (like Etsy, Shopify)

- Restaurant Owners

Platforms

Platform like

- Uber

- Etsy

- Jobber

- Touchbistro

Underwriting

Compliance

Customer Support

Program Manager

Slate can help you with

- Underwriting

- Compliance

- Customer Support

- API's

Bank

Partner Bank/Lender

Bank Lender like

- Peoples Trust

- Meridian

- Cypress Hills

- Merchant Opp Fund

Partners

Partners can track progress of capital programs on Slate dashboard, or pull data via API into their own systems

Offer

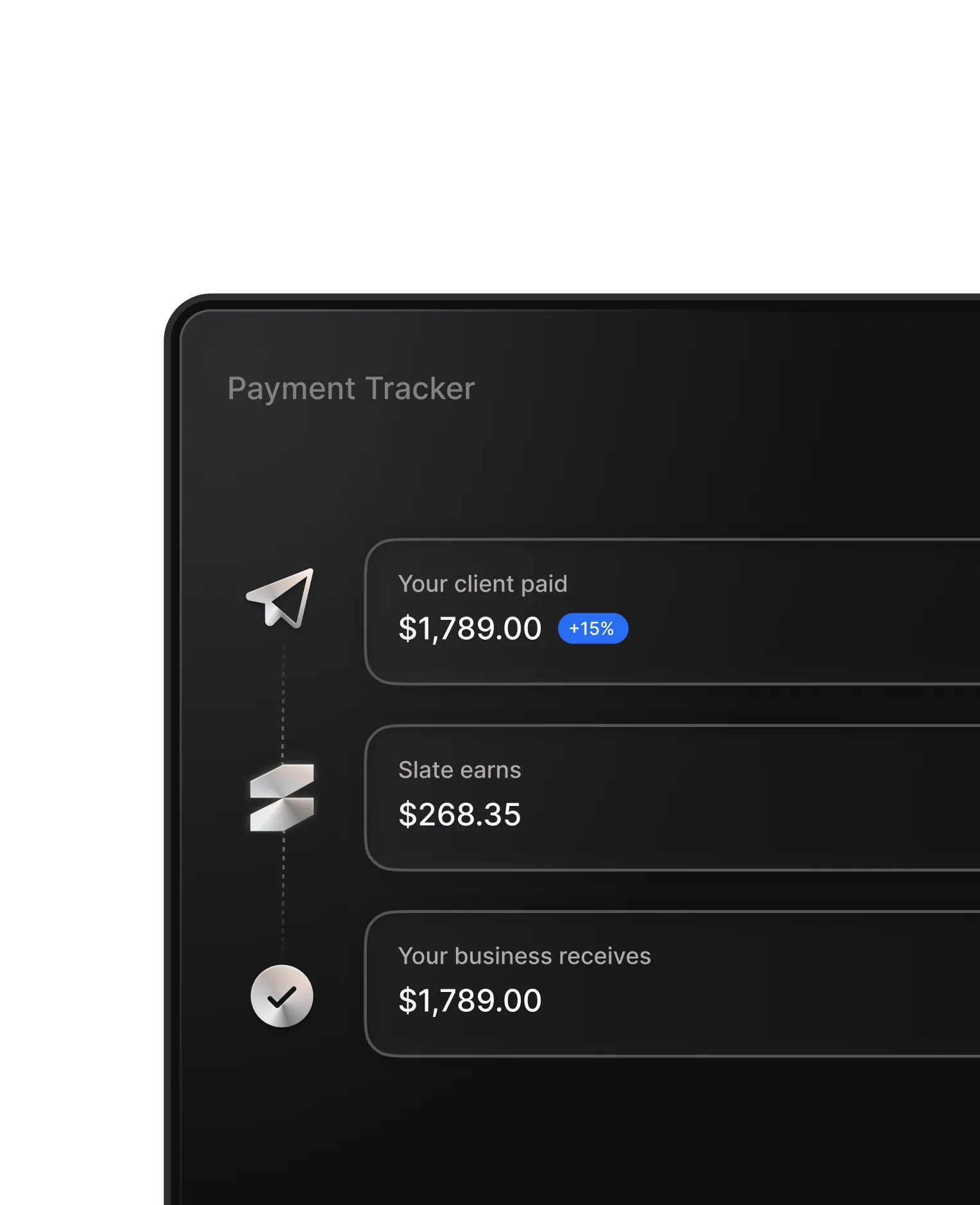

Product experience for small businesses

Slate leverages our partners debt facility to extend capital. Seller is already underwritten and sees the offer in their dashboard

Get Up to $30,000

Your business is pre-approved for $30,000 in working capital

Loan

Slate unlocks embedded lending in Canada

Platforms spend 6+ months and $500K+ to launch lending. Slate helps a platform launch in 24 hours.

Product Offer

Slate continuously underwrites

Slate underwrites the entire customer base of a platform using real-time sales and payments data, powered by AI-driven risk models.

This lets us approve borrowers before they even ask

Allowing us targeting qualified businesses instead of chasing desperate ones with ads.

And because SMEs trust the platforms they run their business on more than banks or alternative lenders,

Slate turns platform trust into seamless, scalable lending

The Team

Meet Scott & Devin

Scott Elliot

10+ Years Across Banks + Fintechs

Co-Founder & CEO

superpower

Turns regulation into competitive moat. A decade of building risk engines across banks and fintechs → knows every step from bank → fintech → hyperscale.

$50M debt facility. Scaled lending ops from $1M → $15M ARR. Negotiated bank partnerships + regulatory engagement

Led Canada expansion. Structured compliance frameworks. Supported U.S. MTL licensing. Closed major B2B platform deals.

Grounded in bank-grade risk + bsa/aml

Scaled compliance + onboarding for thousands of startups. Built the systems that let fintechs move fast without breaking.

Devin Picciolini

10+ Years Launching and Building Digital Products

Co-Founder & CTO

superpower

Turns rejection walls into revenue engines. A 0→1 product leader who knows how to find the pain, hack the workaround, and build the scalable solution.

Led Product for Risk, Compliance & Cards. Issued $50M+ credit, scaled to $15–20M monthly spend, grew customers 200 → 5,000+. Lived the pain that became Slate.

Built & exited a healthtech platform with 25K users and $6.5M+ payments processed.

Product ops at Instagram, scaling ML + infra tools adopted across global teams.

Case Study

We've Done This Before. Now We're Making It Scalable

We built a lending engine at a leading Canadian fintech. 6 months, 15 hires, $500K+. That pain = why Slate exists.

We lived this firsthand

- Core product needed growth → customers needed capital

- Looked for a plug-and-play solution → it didn't exist

- The only option was to build it ourselves

- Chasing borrowers leads to high CAC & poor credit quality.

What we learned

- Lending isn't a feature, its an entire business.

- Most platforms can't afford 6 months, 15 hires, and $500K+ just to get started.

- Just like payments before Stripe, it makes no sense for every platform to reinvent lending.

- U.S. playbooks fail in Canada, borrower behavior + credit profiles are unique to Canada.

- Platforms can cherry-pick the strongest SMEs, Real-time data + loyalty = approve before they even ask.

Business Model

We don't just monetize once. We monetize forever.

Every partner becomes a compounding engine: Setup + ARR + Loan Volume + Servicing → Stickiness → More Partners

$0 - $100K

Setup Fee (enterprise pays, startups free)

15%+

of every loan originated. $1B loan volume = $150M revenue potential

$1M+

per partner LTV

Choose your path

No Engineering

- Pre-approval emails to merchants

- Hosted application flow

- Slate-branded experience

Drop-In Components

- Banner in Helcim dashboard

- White-labeled iframe

- Co-branded experience

Full API

- Native capital experience

- Full white-label

- Custom underwriting data

The Helcim opportunity

The embedded capital wave is here

of Canadian SMEs face ongoing cash flow challenges

originated by Square Loans alone in 2024

higher spend per visit for embedded lending users

50/50 spread share

How Helcim Earns

Projected annual revenue

720 funded merchants x $18K x 2.5 cycles x 10%

Slate Handles Everything

All capital on Slate’s balance sheet

No credit exposure for Helcim

Underwriting & risk assessment

Using Helcim transaction data

Servicing, collections, compliance

Fully managed by Slate

Live in

4 weeks

Launch

- Pre-approval emails sent

- Hosted application flow live

- Revenue starts day 1

Embed

- Banner in Helcim dashboard

- White-labeled iframe

- Co-branded merchant UX

Optimize

- Analyze conversion data

- Tune eligibility criteria

- Expand offer placement

Scale

- Full merchant rollout

- Performance dashboard

- Plan Phase 2 (Full API)

Let's build this together

Confidential · February 2026

Ready to get onboard?

scott@tryslatehq.com

tryslatehq.com